Home » Pensions (Page 2)

Category Archives: Pensions

Will you pay Class 3A NI to top up your Pension?

From 12 October 2015 to 5 April 2017 you’ll be able to make a ‘Class 3A voluntary contribution’ to top up your State Pension by up to £25 per week.

You can choose to top up your State Pension by between £1 and £25 per week. How much you’ll need to contribute depends on:

- how much extra pension you want to get each week

- how old you are when you make the contribution

Example You are 68 years old in October 2015. You decide that you want to get an extra £5 per week (£260 a year) on top of your pension.

The cost of an extra £1 per week for a 68 year old is £827, so you multiply £827 by 5.

You’ll make a lump sum payment of £4,135.

You can use this calculator to see how it works…

https://www.gov.uk/state-pension-topup

Here is a link to the legislation…

http://www.legislation.gov.uk/ukdsi/2014/9780111121689/contents

steve@bicknells.net

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

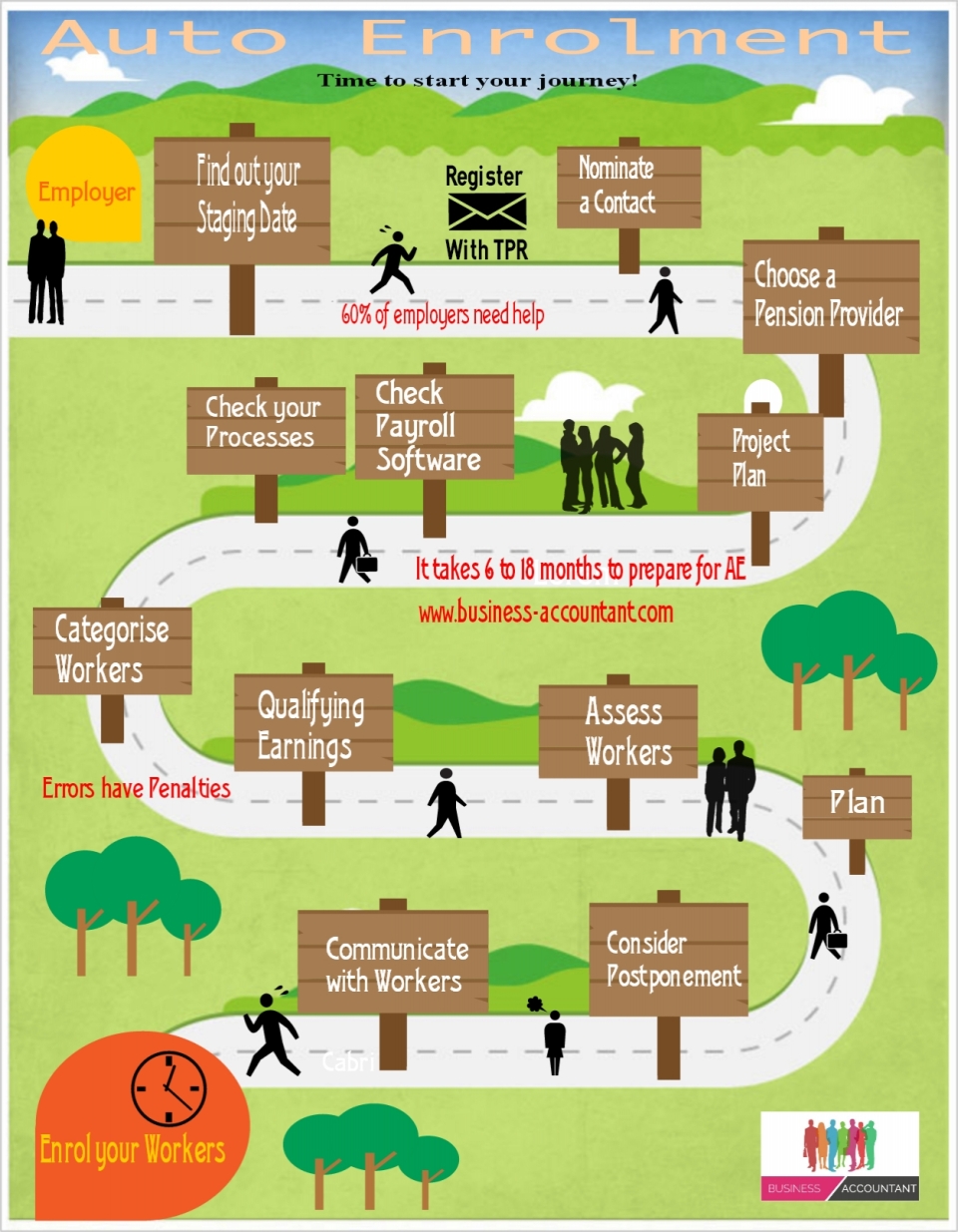

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Have you got a Will?

Currently 47% of UK adults die intestate, in other words without a will.

- Where there are no children, the entire estate will pass to the surviving partner (this shuts out blood relatives such as parents, brothers, sisters or their children)

- Where someone dies leaving a spouse and direct descendants the first £250k will pass to the surviving spouse/partner plus 50 per cent of the remaining balance as a capital sum (previously they had a life interest in 50 per cent of the remaining balance)

- Unmarried couples continue to recieve nothing if their spouse dies intestate

If you are tempted to try a ‘do it yourself’ Will, think again, they might be cheap but the consequences of getting it wrong could be extremely costly for your family.

If you own a business you also need to consider carefully what your succession plan will be.

My advice is to see a solicitor carryout estate planning and prepare a will.

steve@bicknells.net

5 Key Tests the employer must pass to borrow from a Pension Scheme

There are five key tests that a loan from a Pension Scheme must satisfy to qualify as an authorised employer loan. If a loan fails to meet one or more of these tests an unauthorised payment charge will apply.

The five key tests are

- security

- interest rates

- term of loan

- maximum amount of loan and

- repayment terms.

Security [S179, Sch 30]

If a registered pension scheme makes a loan to an employer the amount of the loan must be secured throughout the full term as a first charge on any asset either owned by the sponsoring employer, or some other person, which is of at least equal value to the face value of the loan including interest.

If the asset used as security is taxable property then there may be additional tax charges under the taxable property provisions if the registered pension scheme is an investment regulated pension scheme.

Taxable property consists of residential property and most tangible moveable assets. Residential property can be in the UK or elsewhere and is a building or structure, including associated land, that is used or suitable for use as a dwelling. Tangible moveable property are things that you can touch and move. It includes assets such as art, antiques, jewellery, fine wine, classic cars and yachts.

Interest Rates [S179, Sch 30]

All loans made by registered pension schemes to employers must charge interest at least equivalent to the rate specified in The Registered Pension Schemes (Prescribed Interest Rates for Authorised Employer Loans) Regulations 2005 (SI 2005/3449). This is to ensure that a commercial rate of interest is applied to the loan.

The minimum interest rate a scheme may charge is calculated by reference to 1% above the average of the base lending rates of the following 6 leading high street banks:

- The Bank of Scotland

- Barclays Bank plc

- HSBC plc

- Lloyds TSB plc

- National Westminster plc and

- The Royal Bank of Scotland plc.

The average rate calculated should be rounded up as necessary to the nearest multiple of ¼%.

Term of Loan [S179, Sch 30]

The repayment period of the loan must not be longer than 5 years from the date the loan was advanced. The total amount owing (including interest) must be repaid by the loan repayment date.

Maximum Amount of Loan [S179, Sch 30]

Section 179 (1)(a) of Finance Act 2004 restricts the amount of a loan which can be made to a sponsoring employer to 50% of the aggregate of the amount of the cash sums held and the net market value of the assets of the registered pension scheme valued immediately before the loan is made. These restrictions are necessary because although such loans provide a useful source of business funding, there may be liquidity problems for the scheme if there is a sudden requirement to provide scheme benefits. It may also not be prudent to lend scheme funds to one company.

Repayment Terms [S179, Sch 30]

All loans to employers must be repaid in equal instalments of capital and interest for each complete year of the loan, beginning on the date that the loan is made and ending on the last day of the following 12 month period – known as a loan year.

Often Land and Commercial Property are used as the security for Pension Scheme loans but the problem is having first charge over the asset!

steve@bicknells.net

10 of the Biggest Headaches of Auto Enrolment for Employers

According to Now Pensions the 10 biggest headaches faced by employers are:

- An administrative nightmare – it doesn’t have to be nightmare provided you plan ahead and get help if you need it, accountants are the most used source of help and advice.

- Will payroll be able to cope? Yes but it takes planning and preparation

- A Communication challenge – Employees find pensions complicated and auto enrolment could be the first long tem savings product they have, so simplicity is crucial. Auto Enrolment does require the right correspondence at the right time, so make sure you get it right!

- Future Liabilities – The Pension Regulator enforces compliance and employers must not encourage or put pressure on employees to opt out.

- Middleware – this is software that makes your IT systems talk to each other, many SME’s will not need middleware as the payroll software will do the job of reporting the data to the pension provider

- Responsibility – Make sure you know where the responsibilities fall on your team, mistakes can be costly

- Existing Schemes – Not all existing schemes will be suitable for auto enrolment, check that your scheme will comply or change it

- Investment – Most employees will have never invested in their lives so its important to choose an auto enrolment provider who can help them decide on which funds to invest in

- Value for Money – NEST, Now Pensions and The People Pensions have very low charging structures

- What will it cost – Don’t forget the internal management costs when you choose a scheme, how easy will it be to operate?

steve@bicknells.net

We hear many of the same concerns about auto enrolment being raised on a regular basis in our discussions with employers of all sizes. So you’re not alone with your auto enrolment concerns. That’s why we’ve addressed ten of the biggest headaches and their remedies below.

1: An administrative nightmare

Get all the help you can before the staging date. Employers can lighten the load by partnering with providers that will do much of the work for them. Some pension providers have invested in technology that can automate the administration of auto-enrolment. This includes assessing which sort of scheme is most suitable for your workforce, working out which employees need to be automatically enrolled and calculating contributions and issuing communications to your employees based on the outputs of the assessment.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

2: Will payroll be able to cope?

Yes, provided you make sure the correct people at your payroll provider and your pension provider are talking to each other and exchanging data in the right format.

A strategic decision is necessary to decide on whether payroll will handle employee categorisation ensuring that your auto-enrolment obligations are met compliantly or whether your pension provider will do this. Larger payroll providers and pension providers such as ourselves have the capability to create a record to demonstrate to the Pension Regulator that you have fully complied with your auto-enrolment obligations.

3: A Communications challenge

Employees find pensions complicated, and for many individuals an auto-enrolment pension will be the first long-term savings product they have ever held. So simplicity is crucial.

Research has shown that messages work best when they speak to employees in a language they understand, through a medium via which they like to be communicated. Messages delivered in the run-up to auto-enrolment are particularly important as they will set the agenda for the entire project. So think about what will work best for your workforce. A wealth of compliant communication material that can be tailored to the needs of your workforce is available at no cost from quality pension providers.

4. Future liabilities

The Pensions Regulator enforces compliance with the auto-enrolment rules, and one of its top priorities is ensuring employers do not encourage or put pressure on employees to opt out of the pension scheme after they have been automatically enrolled into it. It will be scrutinising employers that have unusually high opt-out rates. Employers that persistently break the rules by inducing staff to opt-out can be fined up to £10,000 a day. The Pensions Regulator is hoping whistleblowers will report it of breaches of auto-enrolment regulations.

Using compliant communication materials can alleviate the risk of regulatory action. Employers that use pension providers with auto-enrolment middleware will also have a report that demonstrates to the Pensions Regulator that auto-enrolment obligations have been fulfilled, although it will only be as accurate as the information given by the employer.

5: What is ‘middleware’?

Middleware is software that glues different IT systems together. In the context of auto-enrolment, that means analysing the age and salary data of your workforce, working out the earnings upon which contributions are based, taking deductions through payroll and paying them over to the pension provider.

6: Responsibility

For auto-enrolment to run smoothly both your payroll and pensions departments need to talk to each other. Unfortunately the fact that auto-enrolment crosses both areas can lead to confusion over who is responsible for what part of the process. This is best addressed by assigning auto-enrolment to a corporate sponsor high enough up in your organisation to ensure that responsibility for tasks is clearly apportioned, and delegating someone to be involved through the implementation project phase and beyond.

7: Existing Schemes

This will depend on the sort of scheme you have and how you decide to include your  current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

You will need to make some important decisions about how you design your pension offering for the rest of your staff. Do you want a single scheme for everyone in the organisation? Do you want a multifaceted scheme for your senior staff and a more basic scheme for other tiers of your workforce? You may choose to preserve your existing scheme for those already in it, while automatically enrolling those not currently in it into a new scheme. Independent Financial Advisers or Employee Benefit Consultants can provide information and advice in exchange for a fee or Providers like NOW: Pensions can help you to analyse your workforce and provide suggestions based on our previous experience.

8: Investment

Many employees will have never invested this way before in their lives. Poor performance will not only create disgruntled employees – it will also leave some staff with pensions so low they cannot afford to retire when they get older. So choosing the right default investment fund is crucial for an employer.

The performance of different pension providers’ default funds varies hugely. Pensions are long-term savings vehicles which means that even very small increases in performance can make a significant difference. For example, over a 40-year investment, an annual return of 7% will deliver a fund 30% higher than one achieving 6%.

Look for a default fund with a proven track record, one that has delivered stable returns over a long period of time and in different market conditions, and is unlikely to have changed as this may increase the associated communication costs with your employees.

9: Value for money

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

admin fee (£0.30 for low earners during the initial phasing process). For a 25-year-old earning £26,000 saving 8% of salary for 40 years, that can mean the difference between building up a pot of £716,000 rather than the £547,000* generated in a scheme charging 1.5%. Our low charge scheme gives the saver in this example 30% more pension for exactly the same contributions. It may sound hard to believe, but the more expensive provider takes an extra £169,000 in charges out of the saver’s pot.

*Assumes salary increases by 4% a year, fund increases by 7% a year.

10: What will it cost me?

The overall cost of auto enrolment will depend on where you go for your pension and what you need from your pension.

Costs not only include fees and charges but also, human resources and administration so it is important to bear the overall cost in mind when choosing a pension provider. With NOW: Pensions, the employer can either choose to pay nothing in the way of administration with the fees coming from the members or you may choose to pay these fees for your members (employees); on-going costs such as communications are minimal and there are no set-up fees.

It is important to get your provider right from the start as changing further down the line will incur many additional costs.

– See more at: http://www.nowpensions.com/blog/auto-enrolment-headaches/#sthash.HhCRbQuD.dpuf

Is your pension going Dutch?

I love Holland but are their Collective pensions better than ours?

Collective funds pool all contributions into one big fund, so the administration costs are lower and pensions are paid from the fund rather than having to buy annuities.

By running funds collectively rather than individually (the British model) costs are reduced.

Some experts suggest that savers will increase their investment returns by 30%.

An article in the Telegraph 3rd June 2014 commented…

What is certain is that the schemes are a long way from the final salary “gold standard”. There are no guarantees, not even the certainty of a fixed income that you get with an annuity. You may get inflation-linked increases, you may not.

Assuming that these schemes do become available in the coming years, the best course for most workers would probably be to use them for some, not all, of their pension savings, with the rest in traditional schemes, self-invested pensions or Isas.

But will they ever see the light of day? There is little incentive for companies to back them – finance directors remember what happened with final salary schemes, which drove many firms to the brink of bankruptcy thanks to endless “gold-plating”.

So will your pension be going Dutch?

steve@bicknells.net

Are you waiting for a New ISA?

From 1st July 2014, individual savings accounts (ISAs) will be reformed into New ISAs (NISAs) with an annual limit of £15,000.

You can invest your NISA in Cash, Stocks and Shares or in any combination.

The limits for Junior ISAs and Child Trust Funds have already been increased from £3,700 to £4,000.

From July, restrictions on corporate bonds and gilts will have the 5 year rule removed allowing you to invest in short dated securities such as Retail Bonds.

There are plans to enable Peer-to-Peer loans to be held in NISA’s but that’s still in the consultation stage.

Between now and July the most you can invest in an Cash ISA is £5,940.

So are you waiting for a New ISA?

steve@bicknells.net

My staff want to Opt Out of Auto Enrolment…

Not every employee will want to be in Auto Enrolment, for example they may have their own pension arrangements.

But be very careful that you don’t induce or encourage them to opt out.

Most employees will want to be IN

Once staff have been enrolled into the pension scheme, they have one calendar month during which they can opt out and get a full refund of any contributions. This is known as the ‘opt-out period’. It starts from the whichever date is the later of:

- the date active membership was achieved, or

- the date they received your letter with the enrolment information.

Staff can’t opt out before the opt-out period starts or after it ends. If they decide to leave the scheme outside this period, they will instead be ‘ceasing active membership’. Whether they get a refund of contributions will depend on the pension scheme rules.

Staff opt out by giving you an ‘opt-out notice’. The opt-out notice is provided by the pension scheme. This is to avoid any employer involvement in the decision to opt out, which could lead to a breach of the law.

If an employer does anything to encourage or induce an employee or potential employee (at interview) to opt out they will be subject to harsh penalties.

If an employee does Opt Out they will be re-enrolled every 3 years.

steve@bicknells.net

5 reasons to move business premises into your pension?

Often business premises are owned by the business, this could be for many reasons for example the business has multiple owners or it helps to increase the business net worth.

But in many cases it would be better for the premises to be owned by the business owners pension fund because:

- The object of the business is not to own its own property, the objective should be for the business to make profits from trading

- The business could use cash tied up in the premises to invest in trading activities

- Pensions are a very tax efficient method of ownership – no capital gains, no tax on rental profits

- Company Pension Contributions are Tax Deductible and Individual contributions get income tax refunds

- You may be able to use 3 year Carry Forward to get funds into your pension scheme

In summary to move your business premises from your business to a SIPP or SSAS pension you would do the following:

- Find a lender prepared to lend a third of the property value to your pension scheme (which will be half the value of the fund ie if the property was valued at £300k, your pension could borrow £100k which is 50% of the £200k which will need to be funded by your pension scheme)

- Have the premises independently valued and rent assessed and appoint solicitors

- Create a SSAS or SIPP pension (you can include other people in your SSAS or SIPP investments)

- Transfer into your SSAS or SIPP any funds you have in other pension schemes

- As you are the business owner and its your pension scheme your business could make a payment into your pension scheme, the maximum for the last 3 years would be £140k (£50k + £50k + £40k) see details of NRE

- The pension contribution from your company could be an In Specie payment (meaning its in kind not cash)

- You could make a personal payment to your pension and if you are a higher rate tax payer your will get a tax refund via your self assessment return

- Then your pension scheme buys the premises from your business and rents it back to the business

steve@bicknells.net