Home » Employees (Page 3)

Category Archives: Employees

Simplified Expenses – Working From Home

Most people working from home were claiming the £4 per week allowance based on HMRC guidance, but this has now been updated for the self employed.

You can now calculate your allowable expenses using a flat rate based on the hours you work from home each month.

This means you don’t have to work out the proportion of personal and business use for your home, eg how much of your utility bills are for business.

The flat rate doesn’t include telephone or internet expenses. You can claim the business proportion of these bills by working out the actual costs.

You can only use simplified expenses if you work for 25 hours or more a month from home.

| Hours of business use per month | Flat rate per month |

|---|---|

| 25 to 50 | £10 |

| 51 to 100 | £18 |

| 101 and more | £26 |

Example

You worked 40 hours from home for 10 months, but worked 60 hours during 2 particular months:

10 months x £10 = £100

2 months x £18 = £36

Total you can claim = £136

Use the simplified expenses checker to compare what you can claim using simplified expenses with what you can claim by working out the actual costs.

https://www.gov.uk/simpler-income-tax-simplified-expenses/working-from-home

Alternatively you could claim you can claim a proportion (based on the number of rooms and hours of business use) of your household expenses

- Mortgage interest or rent

- Council tax

- Water rates

- Repairs and maintenance

- Building and contents insurance

- Electricity

- Gas, oil or other heating costs

- Cleaning

- Telephone (based on usage)

- Broadband

You can draw up a home rental agreement to reclaim these costs.

The Rental Agreement can be very basic, it just needs to show:

- The Parties – Employee, Company, Home Office Address

- The agreement is for use of the accommodation, furniture etc (‘the Home Office’)

- The hours it will be used

- The rental charge

or your could use an agreement like this one

https://www.rocketlawyer.co.uk/documents-and-forms/home-office-space-agreement.rl#

If the rental is only to cover costs (and not to make a profit) then it should not create any tax liability.

Some experts say that claiming Mortgage Interest and Council Tax can be queried but that would depend on circumstances.

There are also other isuues to consider such as VAT and Capital Gains and these are covered in the blog below.

http://stevejbicknell.com/2013/01/06/what-are-the-tax-issues-and-advantages-of-a-home-office/

steve@bicknells.net

What a difference a day makes

How about three extra days?

HMRC has relaxed the rules on “Real Time Information” for payroll reporting. UK employers are required to send electronic reports to HMRC with each payment of wages to employees. HMRC are now saying that you can submit your RTI report up to three days after the payment date without incurring a penalty.

Any employer who has received an in-year late filing penalty for the period 6 October 2014 to 5 January 2015 and filed within three days, should appeal online by completing the “Other” box and add “Return filed within 3 days”.

Outsource your payroll

Despite the relaxation provided by three extra days, the burden on employers is only likely to increase over the coming months. Auto enrolment is being rolled out to all UK employers over the next couple of years. With the new payroll year about to start on 6th April, now is a good time to consider using a payroll bureau – or at least checking that your current systems will deal effectively with auto enrolment pensions. For more information please and see how Alterledger can help please click here.

Related articles

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

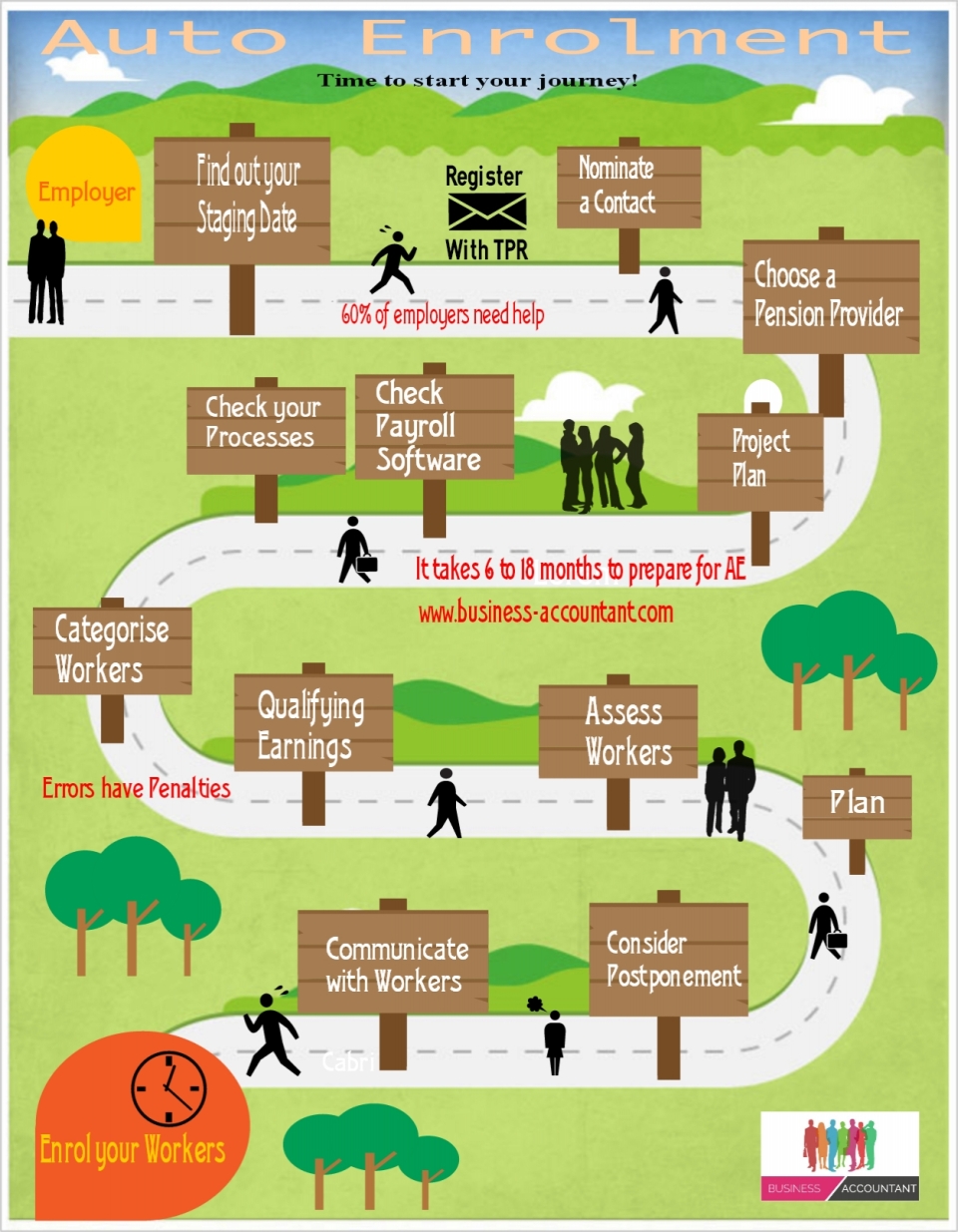

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

How far would you go to retain staff?

Apple and Facebook are now offering to pay for female employees to freeze their eggs!

The initiative is part of the so-called “perks arms race” as Silicon Valley firms battle to recruit top talent and it is hoped the perk will attract more women into a traditionally male-dominated sector. (Sky News)

Fertility specialist Philip Chenette is quoted as saying “providing egg-freezing coverage for employees can be viewed as a type of payback for women’s commitment in a male-dominated industry where technology firms are often competing to attract female talent” (NBC News)

https://www.pacificfertilitycenter.com/fertility-preservation/

The cost for egg freezing in the US is about $10,000 (£6,200) for every round, as well as $500 or more for storage each year.

Apple also offer assistance with adoption.

Will UK companies soon be offering this perk?

steve@bicknells.net

Would an online IR35 test help?

The Term “IR35” became established following a Budget press release issued by the Inland Revenue on 23rd September 1999. That press release was called “IR35”. At its simplest, IR35 is the way in which the taxman closed a loophole that was allowing many contractors and freelance professionals to avoid paying large amounts of Tax and National Insurance.

In 2012 HMRC put forward the Business Tests but they haven’t been as successful as first thought.

Here are the 12 tests, scores shown in()

- Business premises (10)

- PII (2)

- Efficiency (10)

- Assistance (35)

- Advertising (2)

- Previous PAYE (minus 15)

- Business plan (1)

- Repair at own expense (4)

- Client risk (10)

- Billing (2)

- Right of substitution (2)

- Actual substitution (20)

A score less than 10 is high risk and a score more than 20 is low risk. Fail the test and it could cost you a great deal in tax.

In general the key test tend to be:

- Substitution

- Control

- Financial Risk

HMRC launched the ESI (Employment Status Indicator) a while ago.

The recently published Minutes of the IR35 Forum’s last meeting held on 24th July reveal that HMRC are keen for contractors to be able to assess their employment status by way of the Employment Status Indicator (ESI) tool.

Will this resolve the IR35 Status problems?

steve@bicknells.net

Are Cruise Ship Entertainers Employees?

If they weren’t on cruise ships HMRC would probably argue that they were employees but in the case of cruise ships they argue the opposite.

Pete Matthews (1) Keith Sidwick (2) v Revenue & Customs [2011] UKFTT 24 (TC)

Mr Sidwick was a musician and played piano on a series of cruise ships. Mr Matthews was a juggler, similarly entertaining passengers on cruise ships. Both were subject to a close degree of control by the ships officers but the First-tier Tribunal found that this degree of control was required by the context of a cruise ship.

The First-tier Tribunal concluded that the entertainers were not employees ‘…but earn their living by entering into a series of separate engagements with a number of different cruise lines in a similar way to actors…’

The reason why HMRC argued against employment was to stop a claim for Seafarers Earnings Deductions.

To get the deduction you must:

- work on a ship. Oil rigs and other offshore installations aren’t ships for the purposes of Seafarers’ Earnings Deduction – but cargo vessels, tankers, cruise liners and passenger vessels are

- work all or part of the time outside the UK. This means that for each employment you must carry out duties on at least one voyage per year that begins or ends at a foreign port

- be resident in the UK or resident for tax purposes in a European Economic Area (EEA) State (other than the UK) – find out more by following the link ‘Check your residence status’ in the section below

You get the deduction from your earnings as a seafarer if you have an ‘eligible period’ of at least 365 days that consists mainly of days when you are absent from the UK.

From 6 April 2013 the rules that determine if someone is resident in the UK for tax purposes have been put on a statutory basis. These rules are known as the Statutory Residence Test (SRT).

steve@bicknells.net

Can you claim a tax allowance for clothing?

Employees may be able to get tax relief if they – and not their employer – spend money on any tools or specialist clothing they need to be able to do your job. Employees can go back several years to get the relief – the time you’ve got depends on whether you’ve previously sent in a Self Assessment tax return.

As a general rule an employee can’t get tax relief for the cost of clothing they wear to work – but there are some exceptions. For example, if you work in a sector like the building trade or the metal working industry you’ll have to wear protective clothing like:

- overalls

- gloves

- boots

- helmets

If you must pay for the cost of repairing, cleaning or replacing this type of specialist clothing yourself and your employer doesn’t reimburse you, then you are entitled to tax relief. However, you cannot claim for the initial cost of buying this clothing.

EIM32712 sets out some flat rate expenses that can be claimed and EIM32485 allows £60 per year for laundry.

If you are an employee who wants to claim the laundry allowance you should send HMRC a letter as follows:

Re: Uniform Tax Rebate

I have been employed at……… since….. My job title is ……. and I wear a company uniform.

I am obliged to launder the uniform, which is supplied to me by the company. I therefor wish to claim any payment to cover the laundry costs.

The uniform provided is not suitable to be worn outside of the work environment due to having the company logo on it.

I would like to receive the rebate in the form of a cheque….

Self Employed workers have tried to claim for clothes but whilst HMRC have allowed claims for ‘Uniforms’ and ‘Costumes’ they have rejected claims for everyday clothes.

BIM37910 explains to HMRC Inspectors…

You should disallow expenditure on ordinary clothing worn by a trader during the course of their trade. This remains so even where particular standards of dress are required by, for example, the rules of a professional body.

The case of Mallalieu v Drummond [1983] 57 TC 330 (which is discussed in detail below) established that no deduction is available from trading profits for the costs of clothing which forms part of an ‘everyday’ wardrobe. This remains so even where the taxpayer can show that they only wear such clothing in the course of their profession. It is irrelevant that the person chooses not to wear the clothing in question on non-business occasions, the only question is whether the clothing might suitably be worn as part of a hypothetical person’s ‘everyday’ wardrobe.

Most professionals have to keep up appearances but their clothing costs are not allowable (even where they amount to a quasi uniform as in Mallalieu v Drummond).

The cost of clothing that is not part of an ‘everyday’ wardrobe (for example a nurse’s uniform or evening dress (‘tails’) worn by a professional waiter) faces no such bar to deduction.

You should therefore allow a deduction for protective clothing and uniforms.

This was recently tested by Sian Williams who claimed, unsuccessfully…

In her 2004/05 tax return, a newsreader claimed certain deductions from employment income with the BBC for “travel and subsistence costs”, and “other expenses and capital allowances”.

Of these, the following were in dispute:

- Professional hairdo and colouring £975

- Professional clothing for studio £3,231

- Laundry of professional clothes £325

She also claimed that as a taxpayer she had the right to be treated fairly, HMRC should offer up details of the amounts which had been agreed as allowable expenses for other news readers and entertainers.

See article in the Guardian

steve@bicknells.net

We love Self Employment in UK…..

The UK has seen the fastest growth in self-employment in Western Europe over the past year, according to the Institute for Public Policy Research (IPPR).

The number of self-employed workers rose by 8%, faster than any other Western European economy, and outpaced by only a handful of countries in Southern and Eastern Europe.

The IPPR’s analysis shows that the UK – which had low levels of self-employment for many years – has caught up with the EU average. If current growth continues, it says, the UK will look more like Southern and Eastern European countries which tend to have much larger shares of self-employed workers.

According to Tax Research UK…

Something like 80% of all the new jobs created since 2010 are, in fact, self-employments, and there are a number of things that very significantly differentiate self-employments from jobs.

The first is security: there is none.

The second is durability: vast numbers of new small businesses fail, which is one reason why I doubt the official statistics. I am sure they record the supposed start-ups correctly but seriously doubt if they have properly counted the failures.

Then there is the issue of pay. The evidence is overwhelming that in recent years earnings from self-employment have, on average, declined significantly.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

In summary, why is it attractive to use Self Employed Freelancers?

- Skill is more important than location in many business sectors – we live in world where internet can allow you to work with anyone at anytime, you can now track down the best person to work with even if they live thousands of miles away

- Lower fixed costs – Using Freelancers will lower your fixed costs (in similar way to Zero Hours Contracts), you employ them for a specific project and only pay for what you need so there isn’t any surplus capacity

- Tax advantages – Freelancers run their own business and that means they pay less tax than employees. Employers save tax too, such as Employers NI.

- Competitive Advantage – You can put together a team for a contract rather than finding contracts that fit your workforce, this means you can hire the best.

- 110% Commitment – A Freelancers success and future work depends on them performing to the highest level on every contract, failure is not an option for a successful contractor.

So do you think self employment is good for the UK?

Is it a Van or a Car?

It makes a big difference whether a double cab pick up is treated as Car or a Van for tax purposes, in summary:

- Benefit in Kind on Cars is linked to CO2 where as on a Van its Flat Rate (and could be zero if your private use is insignificant)

- Vans qualify for the Annual Investment Allowance, Cars have restricted Capital Allowances

- You can reclaim VAT on Vans but its much harder to reclaim VAT on cars

HMRC have some guidance in EIM23150….

Under this measure, a double cab pick-up that has a payload of 1 tonne (1,000kg) or more is accepted as a van for benefits purposes. Payload means gross vehicle weight (or design weight) less unoccupied kerb weight (care is needed when looking at manufacturers’ brochures as they sometimes define payload differently).

Under a separate agreement between Customs and the Society of Motor Manufacturers and Traders (SMMT), a hard top consisting of metal, fibre glass or similar material, with or without windows, is accorded a generic weight of 45kg. Therefore the addition of a hard top to a double cab pick-up with an ex-works payload of 1,010 kg will convert the vehicle into a car (net payload reduced to 965 kg). Under this agreement, the weight of all other optional accessories is disregarded. HMRC has also adopted this treatment.

http://www.hmrc.gov.uk/manuals/eimanual/eim23150.htm

A double cab with a payload in excess of 1000kg can still be classified as a car if the taxman dealing with the case decides it is a car. You may have to justify a genuine business need for the vehicle.

steve@bicknells.net