Home » Articles posted by Steve Bicknell (Page 5)

Author Archives: Steve Bicknell

10 ways to pay less VAT

Here are my top 10 ways to pay less VAT

1 Choose the best VAT Scheme for your business

Standard VAT Scheme – on this scheme the VAT is based on tax points from invoices

Flat Rate Scheme – try our calculator

VAT Cash Accounting Scheme – if your turnover is below £1.35m you can account for VAT on a Cash basis, this is particularly helpful if your customers pay you on slower terms than you pay your suppliers

Annual Accounting Scheme for VAT – if your turnover is below £1.35m you could join the Annual Scheme and complete one return for the year but you make either 9 interim payments or 3 quarterly interim payments

Retail VAT Schemes – These are specific schemes aimed at mainly at shops and help to overcome the issues of mixed vat rate goods

VAT Margin Scheme – The margin scheme relates to second hand goods and accounts for VAT on the margin, for example on the sale of cars

2 Claim Pre-registration VAT

When you register for VAT, there’s a time limit for backdating claims for VAT paid before registration. From your date of registration the time limit is:

- 4 years for goods you still have, or that were used to make other goods you still have

- 6 months for services

Be careful not to over claim – see this blog for details http://stevejbicknell.com/2015/06/24/preregistration-vat-confusion/

3 Property Investors might benefit from a Development Company

Property Development is a trade, where as Property Investment isn’t – renting out a residential property is a VAT exempt supply.

If you are planning significant building work, setting up a Development Company or using a building contractor might save VAT.

Assuming you employ a builder…

The VAT Rules are in VAT Notice 708 Buildings & Construction

Your builder may be able to charge you VAT at the reduced rate of 5 per cent if you are converting premises into:

- a ‘single household dwelling’

- a different number of ‘single household dwellings’

- a ‘multiple occupancy dwelling’, such as bed-sits, or

- premises intended for use solely for a ‘relevant residential purpose’

As your builder will be VAT registered, they reclaim the VAT they are charged and then charge you VAT at 5%.

If your business is property rental and you do the work yourself, you can’t take advantage of the 5% rate.

If your Development Company is VAT registered you can reclaim all the VAT.

4 Do you need to charge VAT on Intercompany Charges

There are situations where one company is VAT registered and other related companies are either partially exempt or not registered for VAT, so in these circumstances not charging VAT is an advantage.

The following are not Taxable supplies for VAT:

Common Directors – Notice 700/34 (May 2012)

Joint Employment – Notice 700/34 (May 2012)

Paying a Bill on behalf of an associated business

Insurance

5 Use VAT Groups for Business Acquisition Costs

Basically HMRC disallow Input VAT relating to Investments.

The most well known example of this was when BAA purchased Airport Development Investments Limited in June 2006, the decision was upheld by the Court of Appeal in February 2013.

The BAA VAT group sought to recover the VAT (£6.7m) incurred on the acquisition costs but recovery was refused by HMRC on the basis that they considered ADIL had not made onward taxable supplies, had not demonstrated any intention to make taxable supplies and was not a member of the VAT group at the time costs were incurred.

BAA used an SPV (Ferrovial) to purchase ADIL but did not bring the SPV into the BAA VAT Group until September 2006, 3 months after the acquisition.

The lessons to learn from this are:

- Once you have successfully made the acquisition join a VAT Group immediately and make it clear in correspondence that the SPV intends to join the VAT Group at the earliest opportunity

- Consider not using an SPV

- Buy the Assets instead of the Shares

- Show that the SPV will make taxable management charges

- Consider the scope of the advisors work, HMRC may disallow advice focussed on passively holding shares

6 How Hotels save VAT

Here are some VAT examples for Hotels – HMRC Reference:Notice 709/3 (October 2011) :

The Long Stay Rule

If a guest stays in your establishment for a continuous period of more than 28 days, then from the 29th day of the stay you should charge VAT only on that part of the payment that is not for accommodation.

VAT Exempt Meeting Rooms and Refreshments

Hiring a room for a meeting, or letting of shops and display cases are generally exempt, but you may choose to standard-rate them by opting to tax, see Notice 742A Opting to tax land and buildings.

VAT on Deposits

Most deposits serve as advanced payments, and you must account for VAT in the return period in which you receive the payment. If you have to refund a deposit, you can reclaim any VAT you have accounted for in your next return.

Normally, if you make a cancellation charge to a guest who cancels a booking, VAT is not due, because it is compensation.

7 VAT on Pool Cars

When you buy a car you generally can’t reclaim the VAT. There are some exceptions – for example, when the car is used mainly as one of the following:

- a taxi

- for driving instruction

- for self-drive hire

If you lease a car for business purposes you’ll normally be able to reclaim 50 per cent of the VAT you pay. But you can reclaim 100 per cent of the VAT if the car is used exclusively for a business purpose.

8 Use a Tronc for Tips

Tips are outside the scope of VAT when genuinely freely given. This is so regardless of whether:

• the customer requires the amount to be included on the bill

• payment is made by cheque or credit/debit card

• or not the amount is passed to employees.

Restaurant service charges are part of the consideration for the underlying supply of the meals if customers are required to pay them and are therefore

standard rated.

If customers have a genuine option as to whether to pay the service charges, it is accepted that they are not consideration (even if the amounts appear on the invoice) and therefore fall outside the scope of VAT.

Further information is available from: Notices 700 The VAT guide and 709/1 Catering and takeaway food

9 Get your TOGC right – Transfer of a Going Concern

Normally the sale of the assets of a VAT registered or VAT registerable business will be subject to VAT at the appropriate rate. A transfer of a business as a going concern for VAT purposes (TOGC) however is the sale of a business including assets which must be treated as a matter of law, as ‘neither a supply of goods nor a supply of services’ by virtue of meeting certain conditions. Where the sale meets the conditions then the supply is outside the scope of VAT and therefore VAT is not chargeable.

It is important to be aware that the TOGC rules are mandatory and not optional. So it is important to establish from the outset whether the sale is or is not a TOGC.

The main conditions are:

- the assets must be sold as part of the transfer of a ‘business’ as a ‘going concern’

- the assets are to be used by the purchaser with the intention of carrying on the same kind of ‘business’ as the seller (but not necessarily identical)

- where the seller is a taxable person, the purchaser must be a taxable person already or become one as the result of the transfer

- in respect of land which would be standard rated if it were supplied, the purchaser must notify HMRC that he has opted to tax the land by the relevant date, and must notify the seller that their option has not been disapplied by the same date

- where only part of the ‘business’ is sold it must be capable of operating separately

- there must not be a series of immediately consecutive transfers of ‘business’

The TOGC rules are compulsory. You cannot choose to ‘opt out’. So, it is very important that you establish from the outset whether the business is being sold as a TOGC. Incorrect treatment could result in corrective action by HMRC which may attract a penalty and or interest.

10 Choose the best time to register for VAT

You may decide to voluntarily register to reclaim VAT you have paid out to set up you business or you might decide to wait till you have to register to gain a competitive advantage.

You must register for VAT if:

- your VAT taxable turnover is more than £82,000 (the ‘threshold’) in a 12 month period

- you receive goods in the UK from the EU worth more than £82,000

- you expect to go over the threshold in a single 30 day period

steve@bicknells.net

5 million paid the wrong tax last year – is your tax code right?

As reported last year by the Telegraph –

Five million people may have been billed incorrectly by HMRC.

You’ll find your tax code on:

- your pay slip

- your PAYE Coding Notice – you usually get this a couple of months before the start of the tax year and you may also get one if something has changed but not everyone needs to get one

- form P60 – you get this at the end of each tax year

- form P45 – you get this when you leave a job

Among those most likely to be affected are veterans who have taken a civilian job after leaving the Armed Forces, but who also draw a military pension. Pensioners with two pensions and those who have continued to work part-time after retirement are also more likely to be hit.

Taxpayers, who must complete their self-assessment tax returns before Jan 31, are being warned to check their paperwork again to make sure they are not affected.

Problems arise because various tax offices around Britain are failing to share information about taxpayers’ incomes on a central database.

People with more than one income, whether from pensions, PAYE employment or a mixture of the two, are being allocated their personal tax-free allowance multiple times. It means the tax codes issued for their various income sources are incorrect, so not enough tax is taken. Often the mistakes are discovered by HMRC years later, leading to unexpected tax demands. Telegraph

If you think your Tax Code is wrong you should tell HMRC as soon as possible using online form P2

https://online.hmrc.gov.uk/shortforms/form/P2

You can check how your tax using this HMRC link

https://www.gov.uk/check-income-tax

The most common tax code for tax year 2015 to 2016 is 1060L (£10,600 being the annual income tax free allowance for 2015/16) – in 2014 to 2015 it was 1000L. It’s used for most people born after 5 April 1938 with one job and no untaxed income, unpaid tax or taxable benefits (eg company car).

steve@bicknells.net

How would you implement a new accounting system?

Implementing a major accounting system is big undertaking which needs a lot of planning.

Top Tips for System Implementations:

- Start by drawing up a specification of your requirements – what do you want to achieve with the new system, what is the scope of the system, where will cost savings be made, how could more information lead to better decision making?

- Get Buy In – its really important that the system gets the support of the Senior Management Team and that key staff are given the chance to put forward their ideas and are involved in the project. People are often resistant to change and getting them involved early will breakdown barriers to change.

- Rationalise – changing systems is an ideal chance to look at how can you do things differently and stop doing things that don’t add value, this will also reduce potential customisation requirements

- Allocate time to the project – If you don’t allocate time to the implementation project you will regret it later but that doesn’t mean you need to do everything yourself, budget to bring in temps and consultants to help

- Measure the savings and benefits – make sure you achieve your goals

By using simple project management processes, tools and techniques you can achieve the best results.

Formal methods of project management offer a framework to manage this process, providing a series of elements to manage the project through its life cycle. The key elements consist of:

• Defining the project accurately, systematically clarifying objectives

• Planning the project by splitting it up into manageable tasks and stages

• Executing the project by carrying out actions

• Controlling the project through its stages using project definition as a baseline

• Closing/Handing Over the Project

Beware of letting your accounts become a shambles

It’s not uncommon for Directors and Senior Employees to get behind with their expense claims and paperwork, they are busy people trying to build their businesses and sometimes the paperwork gets put to one side.

But lets consider the recent HMRC case against the Directors of RSL (NorthEast) Ltd. Mr White was Director of RSL and he had a company credit card which he used for business and personal expenses, he travelled extensively on company business. Unfortunately RSL became insolvent, so HMRC assessed Mr White on credit card expenses as a benefit in kind.

Mr White appealed on the basis that he had lent the company large amounts of his own money and any credit card expenses were just a reimbursement.

HMRC argued…

- “Section 203(2) ITEPA does not grant any right to retrospectively make good a benefit. Income tax is an annual tax, and the value of the benefit depends upon what is made good in that tax year.”

- “Any “rewriting” [to reflect the money reimbursed to RSL] would have a retrospective effect on the Company accounts.” HMRC implied that this would not be allowed.

HMRC won the case, but mainly because the accounts were in a terrible shambles!

What can we learn from this?

- Keep good records, don’t put off doing your accounts!

- If you do get behind you do a have a ‘reasonable time to make good’ as noted in HMRC’s manuals http://www.hmrc.gov.uk/manuals/eimanual/EIM21121.htm

How do you switch over to Sage One?

So you’ve made the decision, its time to move to Cloud Accounting and you’ve choosen Sage One, what do you need to do to move your accounts to Sage One?

You need to start by deciding the best time to move, it could be your Year End or the end of VAT Quarter, but its likely to be on the 1st of a month.

Get some help, why not find a Sage One accountant and ask them to help you set up your Sage One, they might even offer you a deal and include your other accounting and tax needs.

Then you need to create your Contacts – Customers & Suppliers.

Then you enter opening balances – for example unpaid supplier invoices.

You also need to set up your Bank Feeds

http://uk.sageone.com/bank-feeds/

http://help.sageone.com/en_uk/accounts/extra-bank-feeds.html

To set up bank feeds

1. Banking > click the required bank account.

2. Manage Bank Account > Connect to Bank.

You enter your closing Trial Balance from your old accounting system on the last day of the month before your Sage One start date.

Keep the records and prints from your old accounting system for reference.

Then you are ready to get started, its all very easy and straightforward, nothing to worry about.

steve@bicknells.net

How do you calculate holiday pay for occasional workers?

Almost all workers are legally entitled to 5.6 weeks’ paid holiday per year (known as statutory leave entitlement or annual leave). An employer can include bank holidays as part of statutory annual leave.

Self-employed workers aren’t entitled to annual leave.

But what if your workers work irregular hours, or are part time, or are casual occasional workers, how can you work out how much paid holiday they are entitled to, well actually its not as hard as you think, its based on an accrual of 12.7% per hour worked, here is a spreadsheet to help you calculate it.

Calculating average hourly rate

To calculate average hourly rate, only the hours worked and how much was paid for them should be counted. Take the average rate over the last 12 weeks. If no pay was paid in any week, count back a further week, so that the rate is based on 12 weeks in which pay was paid.

steve@bicknells.net

2015 in review

The WordPress.com stats helper monkeys prepared a 2015 annual report for this blog.

Here’s an excerpt:

The concert hall at the Sydney Opera House holds 2,700 people. This blog was viewed about 14,000 times in 2015. If it were a concert at Sydney Opera House, it would take about 5 sold-out performances for that many people to see it.

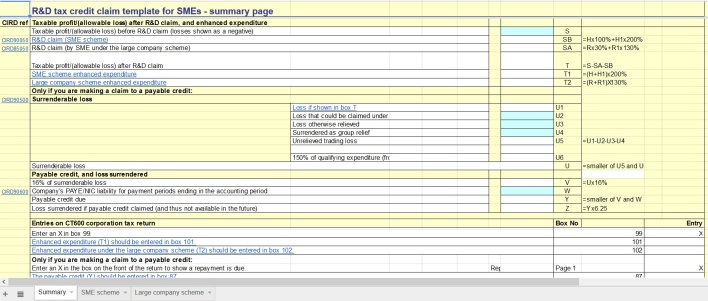

Why aren’t you claiming R&D Tax Credits?

R&D Relief is a Corporation Tax relief that may reduce your company or organisation’s tax bill.

Alternatively, if your company or organisation is small or medium-sized, you may be able to choose to receive a tax credit instead, by way of a cash sum paid by HM Revenue and Customs (HMRC)

But your company or organisation can only claim R&D Relief if it’s liable for Corporation Tax.

The Small and Medium-sized Enterprise Scheme

This scheme has higher rates of relief. Since 1 April 2015, the tax relief on allowable R&D costs is 230% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £130 on top of the £100 spent. It also includes a payable credit in some circumstances.

The Large Company Scheme

If your company isn’t small or medium-sized, then you can only claim under the Large Company Scheme.

Since 1 April 2008, the tax relief on allowable R&D costs is 130% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £30 on top of the £100 spent. If instead there’s an allowable trading loss for the period, this can be increased by 30% of the qualifying R&D costs – £30 for each £100 spent. This loss can be carried forwards or back in the normal way.

Government Statistics show a steady growth in claims

Construction Examples of R&D

- The investigation into the removal of contamination from sites, including land remediation

- Advancements in structural techniques that aid construction relating to unusual ground conditions

- The innovative use of green or sustainable methods and technology

- Development or adaptation of tools to improve efficiency

- The use of new or unique materials, e.g. recycled products

- Improvement on existing construction methods or development of new ideas to solve ongoing issues related to the site environment or project specifications

- Innovative architectural design

IT Systems Examples of R&D

- The design, construction and testing of systems, devices or processes e.g. new hardware or software components, digital interface and control systems

- Integration of legacy and new systems e.g. following a corporate merger or acquisition, the adoption of an Enterprise Architecture or externally with partners in joint ventures

- Advances in network management and operational tools, development of wired or wireless technologies, designing mobile and interactive services, evolution of new generation network switching and control systems

- Data intensive activities e.g. the collection, storage and analysis, distribution and retrieval. Defining or working with new or emerging data models and metadata standards, integration with third party content

These examples and more are shown on the Cost Care Website

There are also examples by Industry on the Alma CG website

http://www.taxdonut.co.uk/blog/2014/12/beginners-guide-claiming-rd-tax-credits-infographic

These are the key questions that you will be asked when requesting an R&D Tax Credit from HMRC:

- How was it decided that R&D had taken place

- A description of the scientific & technological advance sought

- The uncertainties involved

- How and when the uncertainties were resolved

- Why the knowledge being sought was not readily deducible by a competent professional

- Were any grants, subsidies or contributions received for the project within the claim

- Who owns the Intellectual Property of the products resulting from the R&D

- Was the R&D carried out for others ie clients, this could mean your claim is rejected

This HMRC Spreadsheet will help you calculate your Claim

steve@bicknells.net

Business Planning made easy with Apps

A business plan helps you to:

- clarify your business idea

- spot potential problems

- set out your goals

- measure your progress

The problem with Business Plans is that they are time consuming to produce, so business owners put off doing them.

But new Apps might change this and make it much easier to produce high quality Business Plans.

http://www.enloop.com/features

There are other Apps too for example..

steve@bicknells.net

What are the Pros and Cons of Limited Companies?

Click here to access the spreadsheet

What is a Limited Company?

A limited company is an organisation that you can set up to run your business – it’s responsible in its own right for everything it does and its finances are separate to your personal finances.

Any profit it makes is owned by the company, after it pays Corporation Tax. The company can then share its profits.

What is a Sole Trader?

If you start working for yourself, you’re classed as a self-employed sole trader – even if you’ve not yet told HM Revenue and Customs (HMRC).

As a sole trader, you run your own business as an individual. You can keep all your business’s profits after you’ve paid tax on them.

You can employ staff. ‘Sole trader’ means you’re responsible for the business, not that you have to work alone.

You’re personally responsible for any losses your business makes.

The key Advantages and Disadvantages of Companies are shown below.

How do you form a Limited Company?

You can form your company directly with Companies House for £15, it normally takes 24 hours

You’ll need:

- the company’s name and registered address

- names and addresses of directors (and company secretary if you have one)

- details of shareholders and share capital

Personally, I find it easier to use a formation agent such as Company Wizard for £16.99

Often using an agent will mean the company is formed quickly, sometime within a couple of hours.

What are the next steps?

Once your company has been formed you need to:

- Open a bank account for the Company, this can often take a couple of weeks

- Register for Corporation Tax

- Register for other taxes (if they apply to your business) – VAT, PAYE, CIS

- Appoint an accountant (recommended but not compulsory) – Form 64-8

- Set up your accounting software

- Create shareholder agreements, contracts and other legal documents (if required)

steve@bicknells.net