Home » Articles posted by Steve Bicknell (Page 17)

Author Archives: Steve Bicknell

Will your Share Buy Back pass the ‘trade benefit’ test?

Often as part of an exit strategy or succession planning companies will buy back shares.

Setting aside the mechanics, nicely explained in the ACCA Technical Factsheet 177 and the need for S1044 CTA 2010 clearance, the Buy Back has to be in the benefit of the trade not just the shareholder.

For example….

If the purpose is to ensure that an unwilling shareholder who wishes to end his association with the company does not sell his shares to someone who might not be acceptable to the other shareholders, the purchase will normally be regarded as benefiting the company’s trade.

Examples of unwilling shareholders are:

- an outside shareholder who has provided equity finance (whether or not with the expectation of redemption or sale to the company) and who now wishes to withdraw that finance

- a controlling shareholder who is retiring as a director and wishes to make way for new management

- personal representatives of a deceased shareholder, where they wish to realise the value of the shares

- a legatee of a deceased shareholder, where he does not wish to hold shares in the company

Assuming that the shares aren’t being bought back at Par Value, basic rate taxpayers will probably prefer dividends for any surplus where as higher rate taxpayer will want capital treatment.

Share Buy Back is complex, make sure you seek professional advice.

steve@bicknells.net

Why alternative finance could be the key to growth

MarketInvoice is the leading online invoice trading platform. They offer fast, flexible cashflow solutions to help businesses grow. Piers Garthwaite from MarketInvoice talks us through the opportunities alternative finance provides growing businesses.

The problem of funding for growing businesses is an all too common one. For any company to grow it needs medium-term financial support to hire new staff, increase supply, buy more equipment, move to a larger office etc. In this blog, we look at the options your client has to fund their business and why alternative finance could be the key to growth.

There are several ways clients can fund growth for their business:

- invest previous profits back into the business

- take out a loan

- raise equity

- look for other sources of finance

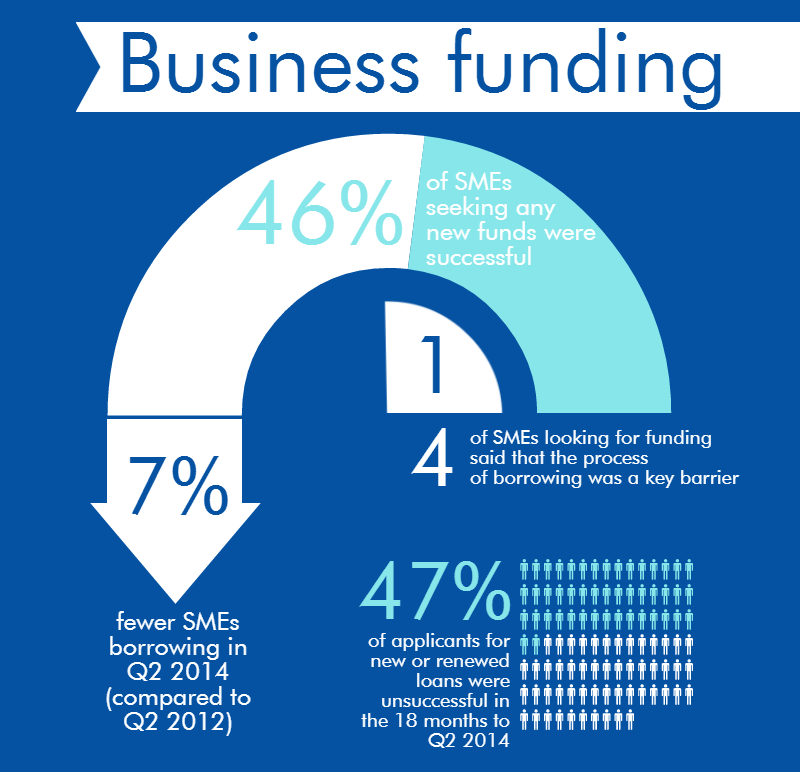

The majority of businesses’ first port of call will be to ask their bank for a loan. As we can see from the infographic, banks are not particularly keen on loans at the moment, given the economic environment.

52% of small businesses say that the availability of credit is “poor” or “very poor” and around half say that credit is unaffordable. In the same period, net lending to SMEs is down at -£400m.

This has been a long-term trend: businesses don’t want the products and banks aren’t keen on offering them. The banks’ policy of belt-tightening has affected growing businesses across the UK.

“So how,” we hear you ask, “am I to help my clients?”

Selling equity instead of a obtaining a loan is one option, but there are a number of disadvantages to this, chiefly your client giving up some control of their company.

Other sources of finance could be a grant, an overdraft (although this is unlikely to be big enough to cover any significant expense), leasing and asset finance, invoice factoring or discounting and, what we will be looking at in this blog, alternative finance.

Firstly, some statistics

The size of the alternative finance market is £1.74 billion. When compared with the banks this is, of course, a drop in the ocean. However, the market has been growing at over 150% year-on-year. The peer-to-peer (P2P) business lending market alone is £750 million and has grown at an average rate of 250% in the past three years. Online invoice trading sits at roughly £300 million, with a growth rate of 174%.

Alternative finance has now matured and is mounting an ever-growing assault on outdated, slow and fee-heavy traditional finance.

The industry-leading Nesta report backs up these findings. 33% of P2P business borrowers believed they would have been unlikely to get funds elsewhere. 63% also said that they saw a growth in profit and 53% saw an increase in employment.

What are the main draws?

For many, the main draws are what define alternative finance against the painful and outdated traditional banking experience:

- Speed: it can still take up to 6 weeks to get a loan. Alternative providers use technology to build automated credit scoring systems. With the amount of data available online, there is no reason for a business to have to wait more than 24 hours to be accepted (or declined) for finance.

- Simplicity and transparency: Standard contracts for bank finance are long and often have charges hidden in the Ts & Cs. Alternative finance tends to be more flexible and more transparent on everything, especially pricing. Most leading alternative finance providers have simple online tools to show how much your client will be charged dependent on the terms you choose.

- Service: Most alternative finance providers are run by entrepreneurs and so they have a natural propensity to understand the concerns and aspirations of small business owners looking to grow their business.

For a growing business to be able to access funding within 24 hours, instead of six weeks, could be crucial to its future success in the modern digital age. Additionally, being able to understand exactly what your clients are getting and at what price will help immensely with financial planning at such a critical stage of a business’ life.

Having explored some of the options available to your client, we hope it’s clear there is a plethora of funding opportunities on offer for small businesses.

You don’t need to be at a loss when considering funding options, even if the banks have said no. Financial support can be fast, simple and accessible and, therefore, the lifeline that a growing business needs at a crucial developmental stage.

If you’d like to find out more, visit MarketInvoice’s website or give them a call on 0845 548 0508.

Twitter: @MarketInvoice and @piersgarthwaite.

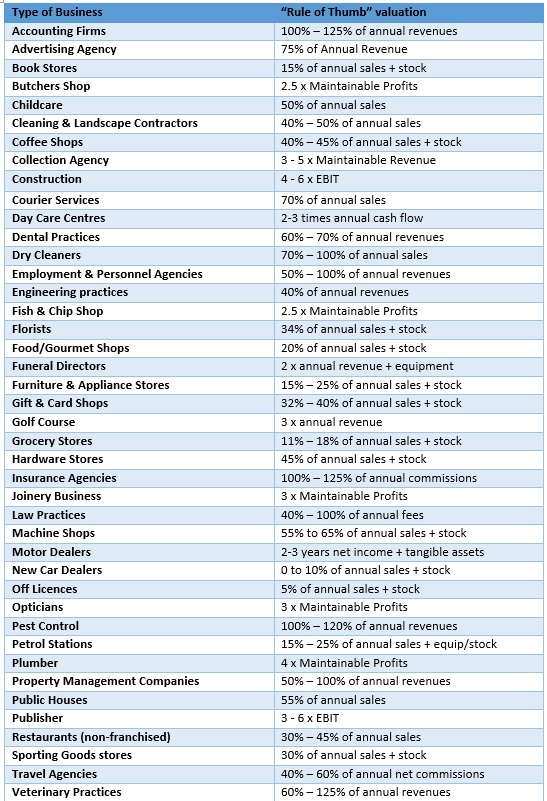

42 Business Valuation “Rules of Thumb” – are they right?

I often get asked for ‘Rules of Thumb’ for small businesses, so I have searched the internet and compiled this list, do you agree with the ‘Rules’?

Rules of Thumb are just a starting point and many other factors need to be considered in valuing a business, it also worth considering HMRC’s views (not so good for Chefs and Hairdressers)..

Any goodwill attributable to the personal skills of the proprietor, for example the personal skills of a chef or a hairdresser, will not be transferred to the new proprietor. Advice should be obtained from the CG Technical Group if it is claimed that the goodwill attributable to the personal skills of the proprietor have been transferred with the business because his/her services have been retained for the foreseeable future by means of an employment contract. All of the relevant facts and circumstances should be established before referral to the CG Technical Group.

http://www.hmrc.gov.uk/manuals/cgmanual/cg68010.htm

steve@bicknells.net

Have you got undeclared Credit Card sales?

The Credit Card Sales Campaign is an opportunity to bring your tax affairs up to date if you’re an individual or business that accepts credit or debit card payments.

Who can do this

This opportunity is for you if:

- you accept card payments for goods or service

- you haven’t declared all your UK tax liabilities

Get the best terms

You need to tell HM Revenue and Customs (HMRC) if you either:

- haven’t registered with them

- have failed to declare all your income

This is called a ‘voluntary disclosure’.

What happens if you should disclose but don’t

HMRC has details of all credit and debit card payments to UK businesses. This information is used to identify individuals and businesses that might not have paid what they owe.

Credit Card Sales Campaign Helpline

Telephone: 0300 123 9272

From outside the UK: +44 300 123 9272

Monday to Friday, 9am to 5pm

steve@bicknells.net

The tax incentive to lend to Social Enterprises?

Social Investment Tax Relief (SITR) came in on 6th April 2014.

Individuals making an eligible investment at any time from 6 April 2014 can deduct 30% of the cost of their investment from their income tax liability for 2014/15 (or the relevant later year in which the investment is made). The minimum period of investment is 3 years.

The income tax and capital gain tax reliefs provide a substantial incentive for investors. To make sure new investment is directed to the organisations which need it most and to meet EU regulations, the investment and the organisation receiving it must meet certain criteria.

Organisations must have a defined and regulated social purpose. Charities, community interest companies or community benefit societies carrying out a qualifying trade, with fewer than 500 employees and gross assets of no more than £15 million may be eligible.

The tax relief is available on unsecured loans as well as shares.

So basically, if you are a basic rate tax payer using SITR will be better than Gift Aid.

Not only do you get the tax relief but if you give a loan it will be repaid (after 3 years).

steve@bicknells.net

Have you got a Will?

Currently 47% of UK adults die intestate, in other words without a will.

- Where there are no children, the entire estate will pass to the surviving partner (this shuts out blood relatives such as parents, brothers, sisters or their children)

- Where someone dies leaving a spouse and direct descendants the first £250k will pass to the surviving spouse/partner plus 50 per cent of the remaining balance as a capital sum (previously they had a life interest in 50 per cent of the remaining balance)

- Unmarried couples continue to recieve nothing if their spouse dies intestate

If you are tempted to try a ‘do it yourself’ Will, think again, they might be cheap but the consequences of getting it wrong could be extremely costly for your family.

If you own a business you also need to consider carefully what your succession plan will be.

My advice is to see a solicitor carryout estate planning and prepare a will.

steve@bicknells.net

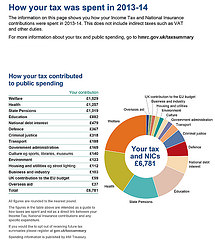

Have you had your annual tax statement?

Back in 2010 the Government promised every taxpayer an annual statement of their tax position – not just the income tax and National Insurance paid, but also where the money was spent.

During October these statement started to be sent out, see the example above.

If you’re registered for online self-assessment you’ll be able to access your statement digitally by logging on to the HMRC website in the usual format, selecting the tax summary option.

Initially the statements will only cover your tax position for 2012/2013 and at first only selected taxpayers will receive one.

Is this a positive step forward or a waste of time?

steve@bicknells.net

Are you one of the third of workers with a part time business?

Almost a third of British workers run some kind of creative business outside their main job contributing an estimated £15bn to the UK economy, according to new research from Moo.com. Profitability among this group of enterprises has increased by 32% in the past year. One in ten part-time creative entrepreneurs plans to leave their job to focus on their business full-time within the next year. However, 60% said it was their passion for the business, and not making money, that motivated them. The most popular part-time creative ventures are in food and cooking, gardening, photography and knitting. (According to Law Donut)

So why are micro businesses taking off:

- You can start off working at home

- Your start up costs are low

- You can do it part time when it suits you

- With wages frozen and costs rising it can provide a useful additional income

- Its easy to be price competitive with low overheads

- The Internet makes it easy to sell your goods and services

- Your social capital can be used to generate sales ie use your contacts and connections

- There could tax advantages – employees generally pay more tax than sole traders

- Some clients prefer the personal touch

- It could be start of something big

Here are my top 20 home based business ideas:

- Get a lodger – Under rent-a-room a taxpayer can be exempt from Income Tax on profits from furnished accommodation in their only or main home if the gross receipts they get (that is, before expenses) are £4,250 or less

- Ironing and Laundry Services – Always popular and you can start with friends and family

- E Bay Trading – as E Bay say… The first task is to sort through those bulging drawers and messy cupboards, finding stuff to flog. Get a big eBay box to stash your wares in, and systematically clear out wardrobes, DVD and CD piles, the loft and garage. Use the easy 12-month rule of thumb to help you decide what to offload: Haven’t used it for a year? Flog it.

- Blogging – Blogging has taken off and many businesses are looking for people to write blogs for them

- Candle Making – You can sell the candles on line and its easy to buy the wax and things you need to make the candles

- Car Boot Sale – As with E Bay but without going on line

- Cake Making – Make sure everything is labelled correctly and you comply with Health & Safety issues

- Data Entry – The internet makes it easy to enter data from where ever you are

- Social Media – Similar to blogging, businesses need help to manage Twitter, Facebook and Linked In

- Website Design – If you have the expertise, go for it

- Sales Parties – Cosmetics to Ann Summers, there is a long list of opportunities

- Sewing and Clothes Alterations – Perfect before and after Christmas

- Jewellery – Making and selling jewellery is always popular and great for Christmas presents

- Car Repairs – Assuming you have the skills needed and comply with legal requirements

- Pet Care – Walking dogs or grooming is popular

- Virtual Assistant – Also personal organiser or personal shopper

- Wedding Planner – You could start by creating a blog about your expertise

- Direct Sales – For example http://www.netmums.com/back-to-work/working-for-yourself/direct-selling-opportunities

- Computer Repair – Great provided you have the skills

- Marketing – Telesales to leaflet design and freelance writing

steve@bicknells.net

TOGC issues on Business Acquisitions

Normally the sale of the assets of a VAT registered or VAT registerable business will be subject to VAT at the appropriate rate. A transfer of a business as a going concern for VAT purposes (TOGC) however is the sale of a business including assets which must be treated as a matter of law, as ‘neither a supply of goods nor a supply of services’ by virtue of meeting certain conditions. Where the sale meets the conditions then the supply is outside the scope of VAT and therefore VAT is not chargeable.

It is important to be aware that the TOGC rules are mandatory and not optional. So it is important to establish from the outset whether the sale is or is not a TOGC.

The main conditions are:

- the assets must be sold as part of the transfer of a ‘business’ as a ‘going concern’

- the assets are to be used by the purchaser with the intention of carrying on the same kind of ‘business’ as the seller (but not necessarily identical)

- where the seller is a taxable person, the purchaser must be a taxable person already or become one as the result of the transfer

- in respect of land which would be standard rated if it were supplied, the purchaser must notify HMRC that he has opted to tax the land by the relevant date, and must notify the seller that their option has not been disapplied by the same date

- where only part of the ‘business’ is sold it must be capable of operating separately

- there must not be a series of immediately consecutive transfers of ‘business’

The TOGC rules are compulsory. You cannot choose to ‘opt out’. So, it is very important that you establish from the outset whether the business is being sold as a TOGC. Incorrect treatment could result in corrective action by HMRC which may attract a penalty and or interest.

Problem areas:

- Gap in trading – for TOGC to apply there must be no significant gap in trading between the sale and purchase

- VAT registration – If the vendor is VAT registered, there can only be a VAT-free TOGC if the purchaser is registered at or before the transfer

- Buying part of a business – the part being bought must be capable of separate operation

- A series of sales – it may not be possible for one of the parties to carry on the trade

- Staged Sales – As long as the overall result is that of business transfer these should qualify for TOGC

steve@bicknells.net

How can you avoid charging VAT on Inter-Company Charges?

There are situations where one company is VAT registered and other related companies are either partially exempt or not registered for VAT, so in these circumstances not charging VAT is an advantage.

The following are not Taxable supplies for VAT:

Common Directors – Notice 700/34 (May 2012)

An individual may act as a director of a number of companies. For convenience one company may pay all the director’s fees and then recover appropriate proportions from the others.

The individual’s services, such as attending meetings or approving expenditure, are supplied by the individual to the companies of which they are a director. The services are supplied directly to the relevant businesses by the individual and not from one company to another. Therefore there is no supply between the companies and so no VAT is due on the share of money recovered from each company.

Joint Employment – Notice 700/34 (May 2012)

Where staff are jointly employed there is no supply for VAT purposes between the joint employers. Staff are jointly employed if their contracts of employment or letters of appointment make it clear that they have more than one employer. The contract must expressly specify who the employers are for example ‘Company A, Company B and Company C’, or ‘Company A and its subsidiaries’.

Paying a Bill on behalf of an associated business

This is basically an inter company loan which will be repayable in full, its not a taxable supply.

Insurance

If insurance is being recharged and both businesses names are on the policy it can be treated as a disbursement of an exempt insurance so that its not vatable.

steve@bicknells.net